In this lab, we will walk through the process of:

Importing real-world financial data from APIs — no more copy-pasting from websites into Excel.

Cleaning and processing messy data that has missing values and formatting issues.

Thinking about data as complete datasets rather than individual cells — the key mindset shift from Excel to Python.

Calculating technical indicators (Moving Averages, Bollinger Bands) to analyze stock trends and volatility.

Implementing a simple trading strategy and backtesting it against historical data.

Building interactive visualizations that let you explore different stocks and time periods.

Important Disclaimer: This lab is for educational purposes only. Stock trading involves significant risk, and past performance does not guarantee future results.

# Run this cell — installs and imports all required packages

try:

import yfinance as yf

except ImportError:

!pip install yfinance

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

import ipywidgets as widgets

from IPython.display import display

import warnings

warnings.filterwarnings('ignore')

%matplotlib inline

print("✓ All libraries loaded successfully!")

✓ All libraries loaded successfully!

1. Importing Stock Data¶

In Excel, getting stock data usually means going to a website, copying a table, and pasting it into a spreadsheet — one stock at a time. In Python, we can download years of data for multiple stocks in a single line of code.

We’ll use the yfinance library, which pulls historical price data directly from Yahoo Finance.

# Run this cell — download 5 years of data for several stocks

tickers = ['AAPL', 'GOOGL', 'MSFT', 'AMZN', 'TSLA']

stock_data = {}

for ticker in tickers:

stock_data[ticker] = yf.download(ticker, period='5y', progress=False)

print(f"✓ {ticker}: {len(stock_data[ticker]):,} trading days downloaded")

# We'll focus on Apple for most of the lab

aapl = stock_data['AAPL'].copy()

print(f"\nDate range: {aapl.index.min().date()} to {aapl.index.max().date()}")

print(f"Total rows: {len(aapl):,}")

✓ AAPL: 1,255 trading days downloaded

✓ GOOGL: 1,255 trading days downloaded

✓ MSFT: 1,255 trading days downloaded

✓ AMZN: 1,255 trading days downloaded

✓ TSLA: 1,255 trading days downloaded

Date range: 2021-03-01 to 2026-02-26

Total rows: 1,255

Let’s look at the first few rows. Notice how the data is organized — each row is a trading day and each column is a measurement. This is fundamentally different from Excel, where you might think about individual cells. In pandas, we think about entire columns at once.

# Run this cell — preview the data

aapl.head(10)

Question 1: How many columns does the stock data have? What does each column represent? How would you describe the difference between “Open” and “Close” price?

Type your answer here, replacing this text.

2. Data Cleaning: Dealing with Messy Real-World Data¶

Real-world data is rarely perfect. Stock data can have missing values (holidays, market closures, data errors), incorrect types, or gaps. Let’s inspect the data quality before we do any analysis.

In Excel, you might scan through rows visually. In pandas, we can check the entire dataset in one command.

# Run this cell — check for missing values across ALL columns at once

print("=== Missing Values per Column ===")

print(aapl.isnull().sum())

print(f"\nTotal missing cells: {aapl.isnull().sum().sum()}")

print(f"Dataset shape: {aapl.shape[0]} rows × {aapl.shape[1]} columns")

print(f"Data types:\n{aapl.dtypes}")

=== Missing Values per Column ===

Price Ticker

Close AAPL 0

High AAPL 0

Low AAPL 0

Open AAPL 0

Volume AAPL 0

dtype: int64

Total missing cells: 0

Dataset shape: 1255 rows × 5 columns

Data types:

Price Ticker

Close AAPL float64

High AAPL float64

Low AAPL float64

Open AAPL float64

Volume AAPL int64

dtype: object

Even if there are no missing values, it’s good practice to check. Now let’s look at basic statistics — the equivalent of using Excel’s AVERAGE(), MIN(), MAX(), and STDEV() on every column simultaneously.

# Run this cell — summary statistics for all columns at once

aapl.describe().round(2)

TO-DO: Sometimes stock data has days where the volume is zero or unusually low, which can indicate data quality issues. Write code to find any days where the trading volume was below 1,000,000 shares.

Hint: Use boolean indexing — df[df['column'] < value]

# TO-DO: Find days with unusually low volume

low_volume_days = aapl[aapl['Volume'] < ...]

print(f"Days with volume below 1,000,000: {len(low_volume_days)}")

low_volume_days[['Close', 'Volume']].head(10)

Question 2: Why might some trading days have very low volume? What could cause this in the real stock market?

Type your answer here, replacing this text.

3. Calculating Daily Returns¶

Before diving into indicators, let’s compute daily returns — the percentage change in closing price from one day to the next. This is a fundamental measure in finance.

In Excel, you’d write a formula like =(B3-B2)/B2 and drag it down. In pandas, one method call handles the entire column.

# Run this cell — calculate daily returns

aapl['Daily_Return'] = aapl['Close'].pct_change() * 100 # as percentage

print("=== Daily Returns (%) ===")

print(aapl[['Close', 'Daily_Return']].tail(10).to_string())

print(f"\nAverage daily return: {aapl['Daily_Return'].mean():.4f}%")

print(f"Std dev of daily returns: {aapl['Daily_Return'].std():.4f}%")

print(f"Best single day: {aapl['Daily_Return'].max():.2f}%")

print(f"Worst single day: {aapl['Daily_Return'].min():.2f}%")

=== Daily Returns (%) ===

Price Close Daily_Return

Ticker AAPL

Date

2026-02-12 261.730011 -4.998181

2026-02-13 255.779999 -2.273340

2026-02-17 263.880005 3.166786

2026-02-18 264.350006 0.178112

2026-02-19 260.579987 -1.426147

2026-02-20 264.579987 1.535037

2026-02-23 266.179993 0.604734

2026-02-24 272.140015 2.239095

2026-02-25 274.230011 0.767986

2026-02-26 272.950012 -0.466761

Average daily return: 0.0777%

Std dev of daily returns: 1.7417%

Best single day: 15.33%

Worst single day: -9.25%

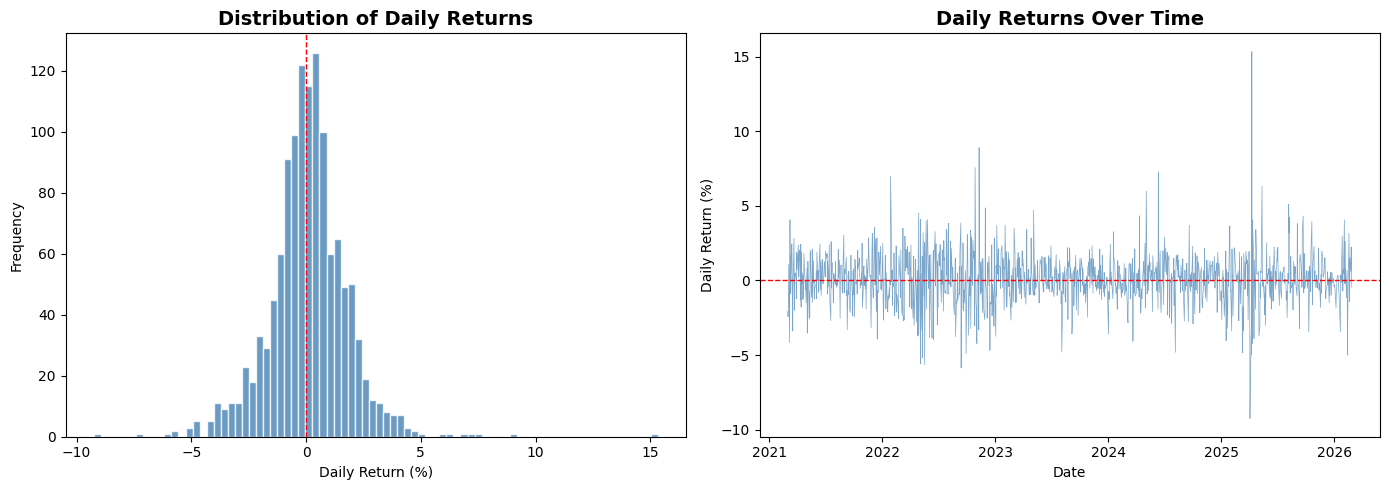

# Run this cell — visualize the distribution of daily returns

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Histogram

axes[0].hist(aapl['Daily_Return'].dropna(), bins=80, color='steelblue', edgecolor='white', alpha=0.8)

axes[0].axvline(x=0, color='red', linestyle='--', linewidth=1)

axes[0].set_title('Distribution of Daily Returns', fontsize=14, fontweight='bold')

axes[0].set_xlabel('Daily Return (%)')

axes[0].set_ylabel('Frequency')

# Time series

axes[1].plot(aapl.index, aapl['Daily_Return'], color='steelblue', linewidth=0.5, alpha=0.7)

axes[1].axhline(y=0, color='red', linestyle='--', linewidth=1)

axes[1].set_title('Daily Returns Over Time', fontsize=14, fontweight='bold')

axes[1].set_xlabel('Date')

axes[1].set_ylabel('Daily Return (%)')

plt.tight_layout()

plt.show()

Question 3: Looking at the histogram, does the distribution of daily returns look symmetric? What does the shape of this distribution tell you about how stock prices move?

Type your answer here, replacing this text.

4. Moving Averages (MA)¶

A moving average smooths out daily price fluctuations to reveal the underlying trend. It’s one of the most widely used tools in technical analysis.

Short-term MA (e.g., 20-day): Reacts quickly to price changes — captures recent trends.

Long-term MA (e.g., 50-day): Slower to react — shows the broader direction.

In Excel, you’d use =AVERAGE(B2:B21) and drag it down, shifting the window one row each time. In pandas, the .rolling() method does this across the entire column.

# Run this cell — calculate 20-day and 50-day moving averages

aapl['MA_20'] = aapl['Close'].rolling(window=20).mean()

aapl['MA_50'] = aapl['Close'].rolling(window=50).mean()

print("Last 10 days with moving averages:")

aapl[['Close', 'MA_20', 'MA_50']].tail(10)

Last 10 days with moving averages:

TO-DO: Add a 200-day moving average to the dataframe. The 200-day MA is commonly used to identify long-term market trends.

# TO-DO: Calculate the 200-day moving average

aapl['MA_200'] = aapl['Close'].rolling(window=...).mean()

# Verify it worked

print("200-day MA (last 5 days):")

print(aapl[['Close', 'MA_200']].tail())

# Run this cell — plot closing price with all three moving averages (last 2 years)

last_2y = aapl.loc[aapl.index >= aapl.index.max() - pd.DateOffset(years=2)]

plt.figure(figsize=(14, 7))

plt.plot(last_2y.index, last_2y['Close'], label='Closing Price', color='black', linewidth=1.2)

plt.plot(last_2y.index, last_2y['MA_20'], label='20-day MA', color='dodgerblue', linewidth=1)

plt.plot(last_2y.index, last_2y['MA_50'], label='50-day MA', color='orange', linewidth=1)

plt.plot(last_2y.index, last_2y['MA_200'], label='200-day MA', color='red', linewidth=1, linestyle='--')

plt.title('Apple Stock Price with Moving Averages', fontsize=16, fontweight='bold')

plt.xlabel('Date', fontsize=12)

plt.ylabel('Price ($)', fontsize=12)

plt.legend(fontsize=11)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

Question 4: When the 20-day MA crosses above the 50-day MA, traders call this a “Golden Cross” — a bullish signal. When it crosses below, it’s a “Death Cross” — bearish. Can you spot any of these crossovers in the chart above? What happened to the price afterward?

Type your answer here, replacing this text.

5. Bollinger Bands¶

Bollinger Bands are a volatility indicator built from three lines:

Middle Band: 20-day Simple Moving Average (SMA)

Upper Band: SMA + 2 × (20-day standard deviation)

Lower Band: SMA − 2 × (20-day standard deviation)

The idea is simple — if the price moves outside the bands, the stock may be overbought (above upper band) or oversold (below lower band). Statistically, about 95% of closing prices should fall within the bands.

In Excel, you’d need separate columns for the SMA, standard deviation, upper band, and lower band — each with a formula dragged across hundreds of rows. In pandas, it’s a few lines.

TO-DO: Calculate Bollinger Bands. Fill in the missing parts:

# TO-DO: Calculate Bollinger Bands

bb_window = 20

# Step 1: Calculate the 20-day SMA (middle band)

aapl['BB_Middle'] = aapl['Close'].rolling(bb_window).mean()

# Step 2: Calculate the 20-day rolling standard deviation

# Hint: Use .rolling(bb_window).std()

aapl['BB_Std'] = aapl['Close'].rolling(bb_window)...

# Step 3: Calculate Upper Band = Middle + 2 * Std

aapl['BB_Upper'] = aapl['BB_Middle'] + (... * aapl['BB_Std'])

# Step 4: Calculate Lower Band = Middle - 2 * Std

aapl['BB_Lower'] = aapl['BB_Middle'] - (... * aapl['BB_Std'])

print("Bollinger Bands (last 5 days):")

aapl[['Close', 'BB_Upper', 'BB_Middle', 'BB_Lower']].tail()

# Run this cell — plot Bollinger Bands (last 2 years)

last_2y = aapl.loc[aapl.index >= aapl.index.max() - pd.DateOffset(years=2)]

plt.figure(figsize=(14, 7))

plt.plot(last_2y.index, last_2y['Close'], label='Closing Price', color='blue', linewidth=1.2)

plt.plot(last_2y.index, last_2y['BB_Middle'], label='SMA (20-day)', color='black', linestyle='--', linewidth=1)

plt.plot(last_2y.index, last_2y['BB_Upper'], label='Upper Band', color='red', linewidth=0.8)

plt.plot(last_2y.index, last_2y['BB_Lower'], label='Lower Band', color='green', linewidth=0.8)

plt.fill_between(last_2y.index, last_2y['BB_Upper'], last_2y['BB_Lower'], color='gray', alpha=0.15)

plt.title('Apple Stock — Bollinger Bands (Last 2 Years)', fontsize=16, fontweight='bold')

plt.xlabel('Date', fontsize=12)

plt.ylabel('Price ($)', fontsize=12)

plt.legend(fontsize=11)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

TO-DO: Identify overbought and oversold days in the last 2 years. Use boolean indexing to find days where the closing price was above the upper band or below the lower band.

# TO-DO: Find overbought and oversold days

# Hint: overbought means Close > BB_Upper, oversold means Close < BB_Lower

overbought = last_2y[last_2y['Close'] ... last_2y['BB_Upper']]

oversold = last_2y[last_2y['Close'] ... last_2y['BB_Lower']]

print(f"Overbought days (last 2 years): {len(overbought)}")

print(f"Oversold days (last 2 years): {len(oversold)}")

if len(overbought) > 0:

print("\nMost recent overbought dates:")

print(overbought[['Close', 'BB_Upper']].tail())

if len(oversold) > 0:

print("\nMost recent oversold dates:")

print(oversold[['Close', 'BB_Lower']].tail())

Question 5: Looking at the Bollinger Bands chart, can you identify any periods where the bands became very wide or very narrow? What does the width of the bands tell you about the stock’s volatility during those periods?

Type your answer here, replacing this text.

6. Trading Strategy: Moving Average Crossover¶

Now let’s combine what we’ve learned into a simple trading strategy and test whether it would have made money historically. This process is called backtesting.

The strategy:

BUY when the 20-day MA crosses above the 50-day MA (upward momentum)

SELL when the 20-day MA crosses below the 50-day MA (downward momentum)

Otherwise, HOLD your current position

This is one of the simplest algorithmic trading strategies. Let’s see how it performs.

TO-DO: Create buy/sell signals based on the MA crossover rule. Fill in the signal values.

# TO-DO: Generate trading signals

# Signal = 1 → BUY / HOLD long position

# Signal = -1 → SELL / SHORT position

aapl['Signal'] = 0

# When 20-day MA is above 50-day MA → bullish → signal = ?

aapl.loc[aapl['MA_20'] > aapl['MA_50'], 'Signal'] = ...

# When 20-day MA is below 50-day MA → bearish → signal = ?

aapl.loc[aapl['MA_20'] < aapl['MA_50'], 'Signal'] = ...

# Detect crossovers: where the signal changes

aapl['Crossover'] = aapl['Signal'].diff()

buy_signals = aapl[aapl['Crossover'] == 2] # -1 → +1 = change of 2

sell_signals = aapl[aapl['Crossover'] == -2] # +1 → -1 = change of -2

print(f"Total BUY signals: {len(buy_signals)}")

print(f"Total SELL signals: {len(sell_signals)}")

# Run this cell — visualize the buy/sell signals on the price chart (last 3 years)

last_3y = aapl.loc[aapl.index >= aapl.index.max() - pd.DateOffset(years=3)]

buys_3y = buy_signals.loc[buy_signals.index >= last_3y.index.min()]

sells_3y = sell_signals.loc[sell_signals.index >= last_3y.index.min()]

plt.figure(figsize=(14, 7))

plt.plot(last_3y.index, last_3y['Close'], label='Closing Price', color='black', linewidth=1)

plt.plot(last_3y.index, last_3y['MA_20'], label='20-day MA', color='dodgerblue', linewidth=0.9)

plt.plot(last_3y.index, last_3y['MA_50'], label='50-day MA', color='orange', linewidth=0.9)

plt.scatter(buys_3y.index, buys_3y['Close'], marker='^', color='green', s=120,

label='BUY Signal', zorder=5, edgecolors='black', linewidth=0.5)

plt.scatter(sells_3y.index, sells_3y['Close'], marker='v', color='red', s=120,

label='SELL Signal', zorder=5, edgecolors='black', linewidth=0.5)

plt.title('Moving Average Crossover — Buy & Sell Signals (Last 3 Years)', fontsize=16, fontweight='bold')

plt.xlabel('Date', fontsize=12)

plt.ylabel('Price ($)', fontsize=12)

plt.legend(fontsize=11)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

Question 6: Look at the buy/sell signal chart. Are there any signals that appear to be “wrong” — for example, a buy signal right before the price dropped, or a sell signal right before a rally? Why might this happen with a moving-average-based strategy?

Type your answer here, replacing this text.

7. Backtesting: Did the Strategy Make Money?¶

Backtesting means applying a trading strategy to historical data to see how it would have performed. We’ll compare:

Buy & Hold: Buy Apple stock at the start and hold for the entire period.

MA Crossover Strategy: Follow the buy/sell signals we just created.

# Run this cell — backtest the MA crossover strategy

# Use last 3 years for the backtest

bt = last_3y[['Close', 'Signal']].copy()

bt = bt.dropna()

# Daily returns

bt['Market_Return'] = bt['Close'].pct_change()

# Strategy return: only earn market return when Signal = 1 (long position)

# When Signal = -1, we assume we're in cash (0% return)

bt['Strategy_Return'] = bt['Market_Return'] * bt['Signal'].shift(1)

# Cumulative returns (growth of $1)

bt['Buy_Hold_Growth'] = (1 + bt['Market_Return']).cumprod()

bt['Strategy_Growth'] = (1 + bt['Strategy_Return']).cumprod()

# Final results

bh_total = (bt['Buy_Hold_Growth'].iloc[-1] - 1) * 100

st_total = (bt['Strategy_Growth'].iloc[-1] - 1) * 100

print("=" * 50)

print(" BACKTEST RESULTS (Last 3 Years)")

print("=" * 50)

print(f" Buy & Hold Return: {bh_total:+.2f}%")

print(f" MA Crossover Return: {st_total:+.2f}%")

print(f" Difference: {st_total - bh_total:+.2f}%")

print("=" * 50)

if st_total > bh_total:

print(" → Strategy OUTPERFORMED buy & hold")

else:

print(" → Strategy UNDERPERFORMED buy & hold")

# Run this cell — plot cumulative growth comparison

plt.figure(figsize=(14, 7))

plt.plot(bt.index, bt['Buy_Hold_Growth'], label='Buy & Hold', color='blue', linewidth=1.5)

plt.plot(bt.index, bt['Strategy_Growth'], label='MA Crossover Strategy', color='green', linewidth=1.5)

plt.axhline(y=1, color='gray', linestyle='--', linewidth=0.8)

plt.fill_between(bt.index, bt['Buy_Hold_Growth'], bt['Strategy_Growth'],

where=(bt['Strategy_Growth'] > bt['Buy_Hold_Growth']),

color='green', alpha=0.1, label='Strategy Winning')

plt.fill_between(bt.index, bt['Buy_Hold_Growth'], bt['Strategy_Growth'],

where=(bt['Strategy_Growth'] <= bt['Buy_Hold_Growth']),

color='red', alpha=0.1, label='Buy & Hold Winning')

plt.title('Growth of $1: Buy & Hold vs MA Crossover Strategy', fontsize=16, fontweight='bold')

plt.xlabel('Date', fontsize=12)

plt.ylabel('Portfolio Value ($)', fontsize=12)

plt.legend(fontsize=11)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

Question 7: Did the MA crossover strategy beat simply buying and holding? Why do you think simple strategies like this often struggle to outperform buy & hold in the long run?

Type your answer here, replacing this text.

8. Risk Analysis¶

Return is only half the picture — we also need to measure risk. A strategy that makes more money but has wild swings may not be better. Let’s compare the risk profiles.

# Run this cell — compare risk metrics

def risk_report(returns, label):

"""Calculate key risk metrics for a return series."""

annual_return = returns.mean() * 252 * 100

annual_vol = returns.std() * np.sqrt(252) * 100

sharpe = (returns.mean() / returns.std()) * np.sqrt(252) if returns.std() > 0 else 0

max_dd = ((1 + returns).cumprod() / (1 + returns).cumprod().cummax() - 1).min() * 100

return {

'Strategy': label,

'Annual Return (%)': f"{annual_return:.2f}",

'Annual Volatility (%)': f"{annual_vol:.2f}",

'Sharpe Ratio': f"{sharpe:.2f}",

'Max Drawdown (%)': f"{max_dd:.2f}"

}

bh_metrics = risk_report(bt['Market_Return'].dropna(), 'Buy & Hold')

st_metrics = risk_report(bt['Strategy_Return'].dropna(), 'MA Crossover')

risk_df = pd.DataFrame([bh_metrics, st_metrics]).set_index('Strategy')

risk_df

Key terms explained:

Annual Volatility: How much the returns fluctuate year-to-year. Lower is more stable.

Sharpe Ratio: Return per unit of risk. Higher is better. Above 1.0 is generally considered good.

Max Drawdown: The largest peak-to-trough decline. This tells you the worst-case scenario — how much you could have lost at the worst possible time.

Question 8: Compare the Sharpe Ratios and Max Drawdowns of both strategies. Even if one strategy has a lower total return, could it still be “better” from a risk perspective? Why might an investor prefer a lower-return strategy with lower risk?

Type your answer here, replacing this text.

9. Interactive Stock Explorer¶

Now let’s put everything together into an interactive tool. Use the dropdown and slider below to analyze different stocks and time windows. The widget calculates Bollinger Bands and identifies overbought/oversold conditions automatically.

# Run this cell — build the interactive stock analyzer

def analyze_stock(ticker, years):

"""Generate Bollinger Band analysis for a given stock and time window."""

df = stock_data[ticker].copy()

cutoff = df.index.max() - pd.DateOffset(years=years)

# Calculate Bollinger Bands on full data, then filter

df['BB_Mid'] = df['Close'].rolling(20).mean()

df['BB_Std'] = df['Close'].rolling(20).std()

df['BB_Up'] = df['BB_Mid'] + 2 * df['BB_Std']

df['BB_Lo'] = df['BB_Mid'] - 2 * df['BB_Std']

df = df.loc[df.index >= cutoff]

overbought = df[df['Close'] > df['BB_Up']]

oversold = df[df['Close'] < df['BB_Lo']]

fig, ax = plt.subplots(figsize=(14, 7))

ax.plot(df.index, df['Close'], label='Close', color='blue', linewidth=1.2)

ax.plot(df.index, df['BB_Mid'], label='SMA (20)', color='black', linestyle='--', linewidth=0.9)

ax.plot(df.index, df['BB_Up'], color='red', linewidth=0.7)

ax.plot(df.index, df['BB_Lo'], color='green', linewidth=0.7)

ax.fill_between(df.index, df['BB_Up'], df['BB_Lo'], color='gray', alpha=0.12)

if len(overbought) > 0:

ax.scatter(overbought.index, overbought['Close'], color='red',

marker='v', s=60, zorder=5, label=f'Overbought ({len(overbought)})')

if len(oversold) > 0:

ax.scatter(oversold.index, oversold['Close'], color='green',

marker='^', s=60, zorder=5, label=f'Oversold ({len(oversold)})')

ax.set_title(f'{ticker} — Bollinger Bands ({years} Year{"s" if years > 1 else ""})',

fontsize=16, fontweight='bold')

ax.set_xlabel('Date', fontsize=12)

ax.set_ylabel('Price ($)', fontsize=12)

ax.legend(fontsize=10)

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

latest = df.iloc[-1]

print(f" Latest Close: ${latest['Close']:.2f}")

print(f" Upper Band: ${latest['BB_Up']:.2f}")

print(f" Lower Band: ${latest['BB_Lo']:.2f}")

status = "OVERBOUGHT" if latest['Close'] > latest['BB_Up'] else \

"OVERSOLD" if latest['Close'] < latest['BB_Lo'] else "NORMAL"

print(f" Current Status: {status}")

# Build widget interface

stock_dropdown = widgets.Dropdown(options=tickers, value='AAPL', description='Stock:')

years_slider = widgets.IntSlider(value=2, min=1, max=5, step=1, description='Years:')

out = widgets.Output()

def on_change(_):

with out:

out.clear_output(wait=True)

analyze_stock(stock_dropdown.value, years_slider.value)

stock_dropdown.observe(on_change, names='value')

years_slider.observe(on_change, names='value')

print("=== INTERACTIVE STOCK ANALYZER ===")

display(widgets.HBox([stock_dropdown, years_slider]))

display(out)

on_change(None)

TO-DO: Use the interactive widget to analyze a stock other than Apple. Answer the following:

Question 9: Which stock did you choose? Is it currently overbought, oversold, or in the normal range? Compare the band width to Apple’s — which stock appears more volatile?

Type your answer here, replacing this text.

10. Your Turn: Analyze a Stock of Your Choice¶

In the cell below, download data for a stock that is not in our original list. You can find ticker symbols on Yahoo Finance.

Complete the following tasks:

Download the data using

yf.download()Calculate 20-day and 50-day moving averages

Calculate Bollinger Bands

Create at least one visualization

# TO-DO: Choose your own stock and perform the analysis

# Step 1: Download data (replace 'NFLX' with any ticker you want)

my_stock = yf.download('...', period='5y', progress=False)

# Step 2: Calculate moving averages

my_stock['MA_20'] = ...

my_stock['MA_50'] = ...

# Step 3: Calculate Bollinger Bands

my_stock['BB_Mid'] = ...

my_stock['BB_Std'] = ...

my_stock['BB_Upper'] = ...

my_stock['BB_Lower'] = ...

# Step 4: Create a plot (at least one visualization)

plt.figure(figsize=(14, 7))

# ... your plotting code here ...

plt.show()

Question 10: Describe what you found for your chosen stock. Does it show different behavior compared to Apple? Would the MA crossover strategy have worked better or worse on this stock? What might explain the differences?

Type your answer here, replacing this text.

11. Reflection: Excel vs Python for Data Analysis¶

Question 11: Based on your experience in this lab, list at least 3 advantages of using Python/pandas for stock analysis compared to doing the same work in Excel. Then list at least 1 situation where Excel might still be preferable.

Type your answer here, replacing this text.

Question 12: Think about the backtesting process. In Excel, you’d need to write formulas row-by-row, then manually calculate cumulative returns. In Python, we did it in a few lines. How does this relate to the concept of automation in data analysis?

Type your answer here, replacing this text.

Bonus Challenge (Optional)¶

Try to improve the MA crossover strategy. Some ideas:

Different MA periods: Instead of 20 and 50, try 10 and 30, or 50 and 200. Does performance change?

Add a volume filter: Only trade when volume is above its 20-day average.

Combine indicators: Use both MA crossover and Bollinger Bands — for example, only buy when the MA signal is bullish AND price is near the lower Bollinger Band.

Test multiple stocks: Run your strategy on all 5 stocks and compare results.

# Bonus: Experiment with strategy improvements here

Summary¶

In this lab, you learned to:

✓ Import live stock data using Python APIs — replacing manual copy-paste from websites

✓ Clean and inspect data quality across an entire dataset at once

✓ Calculate daily returns, moving averages, and Bollinger Bands

✓ Implement a trading strategy and backtest it against historical data

✓ Measure risk using volatility, Sharpe Ratio, and maximum drawdown

✓ Build interactive visualizations for exploring different stocks

Key takeaway: Python and pandas let you work with data as complete sets — calculating indicators across thousands of rows simultaneously, automating repetitive analysis, and testing ideas that would take hours to set up in Excel. This is the foundation of data-driven decision making.

Important reminder: This lab is for educational purposes only. Real stock trading involves significant financial risk. Always consult a qualified financial advisor before making investment decisions.